Supportive Headlines, Heavy Fundamentals

Jun 01, 2026

Zack Gardner

Grain Marketing & Origination Specialist

What has changed in the last two months?

In the two months since our April grain update (written at the end of March), I don’t think anything has really changed. As of this writing, December corn is only off $0.12 since our last e-newsletter in April.

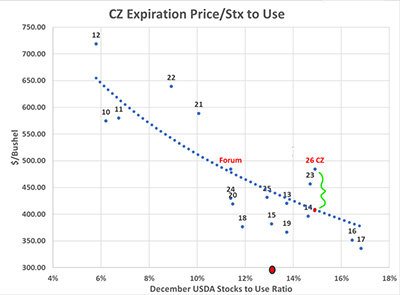

Fundamentally speaking, we have had a decent swath of what would normally be market moving adjustments such as the May USDA report giving us a corn carryout number below the psychological 2-billion-bushel mark, or the USDA raising Argentina’s corn production number by 7 MMT (275 million bushels), and Brazil’s corn production by 3 MMT (118 million bushels). But the market is still focused on the Middle East and the funds traders are buying all commodities as an inflation hedge. I think this chart from two months ago still applies, showing that we are still fundamentally overpriced.

Click to view graph.

What happens next and what’s our risk?

As of the last funds traders’ position report, the funds are currently long 293,000 contracts of corn, which isn’t too far from their record of 364,217 contracts. We are starting to hear more rumors and see more headlines about a potential 60-day ceasefire deal with Iran. With the funds as long as they are, I think we have more risk to the downside than the upside. If we do get a ceasefire or a resolution in the Middle East, crude oil might sell off and drag corn and soybeans down with it.

I still lean bearishly long term, but in the last two months I’ve become less bearish. Not bullish, just less bearish. On the summer acreage report, I do think we will see some corn acres switch to soybeans as well as some corn acres out west go to prevent plant from dryness. Just throwing numbers out there, but if we lose 1.5 million corn acres, that’d take roughly 250 million bushels of corn off our balance sheet. Our carryout would go from 1.957 billion bushels to roughly 1.75 billion. Friendlier, yes, but a 1.75-billion-bushel carryout still doesn’t correlate to $4.82 December futures.

Grain Marketing & Origination Specialist

What has changed in the last two months?

In the two months since our April grain update (written at the end of March), I don’t think anything has really changed. As of this writing, December corn is only off $0.12 since our last e-newsletter in April.

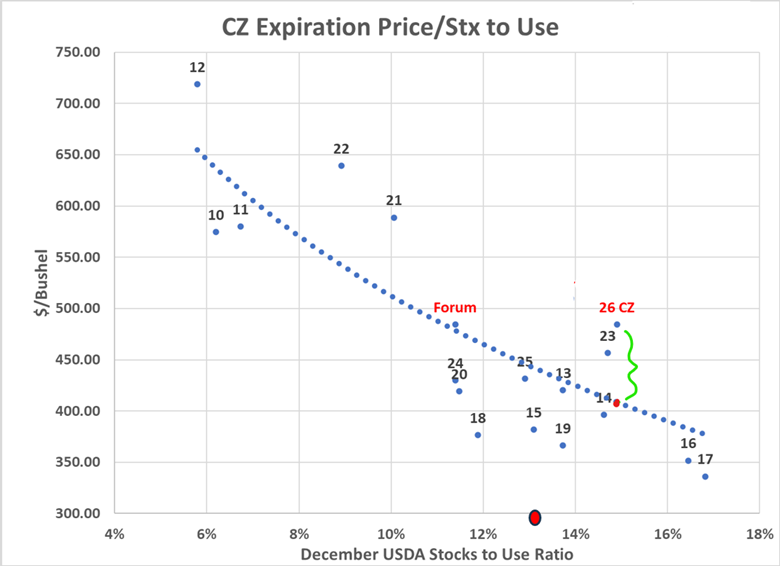

Fundamentally speaking, we have had a decent swath of what would normally be market moving adjustments such as the May USDA report giving us a corn carryout number below the psychological 2-billion-bushel mark, or the USDA raising Argentina’s corn production number by 7 MMT (275 million bushels), and Brazil’s corn production by 3 MMT (118 million bushels). But the market is still focused on the Middle East and the funds traders are buying all commodities as an inflation hedge. I think this chart from two months ago still applies, showing that we are still fundamentally overpriced.

Click to view graph.

What happens next and what’s our risk?

As of the last funds traders’ position report, the funds are currently long 293,000 contracts of corn, which isn’t too far from their record of 364,217 contracts. We are starting to hear more rumors and see more headlines about a potential 60-day ceasefire deal with Iran. With the funds as long as they are, I think we have more risk to the downside than the upside. If we do get a ceasefire or a resolution in the Middle East, crude oil might sell off and drag corn and soybeans down with it.

I still lean bearishly long term, but in the last two months I’ve become less bearish. Not bullish, just less bearish. On the summer acreage report, I do think we will see some corn acres switch to soybeans as well as some corn acres out west go to prevent plant from dryness. Just throwing numbers out there, but if we lose 1.5 million corn acres, that’d take roughly 250 million bushels of corn off our balance sheet. Our carryout would go from 1.957 billion bushels to roughly 1.75 billion. Friendlier, yes, but a 1.75-billion-bushel carryout still doesn’t correlate to $4.82 December futures.